Most people do not think about the Federal Reserve when they pay bills, check mortgage rates, or plan a home purchase. Yet the Fed quietly affects many financial decisions Americans make every single day.

Have you ever wondered why mortgage rates suddenly rise even when home prices stay the same? Or why does your credit card bill feel heavier after a few months? In many cases, the answer connects back to the Federal Reserve.

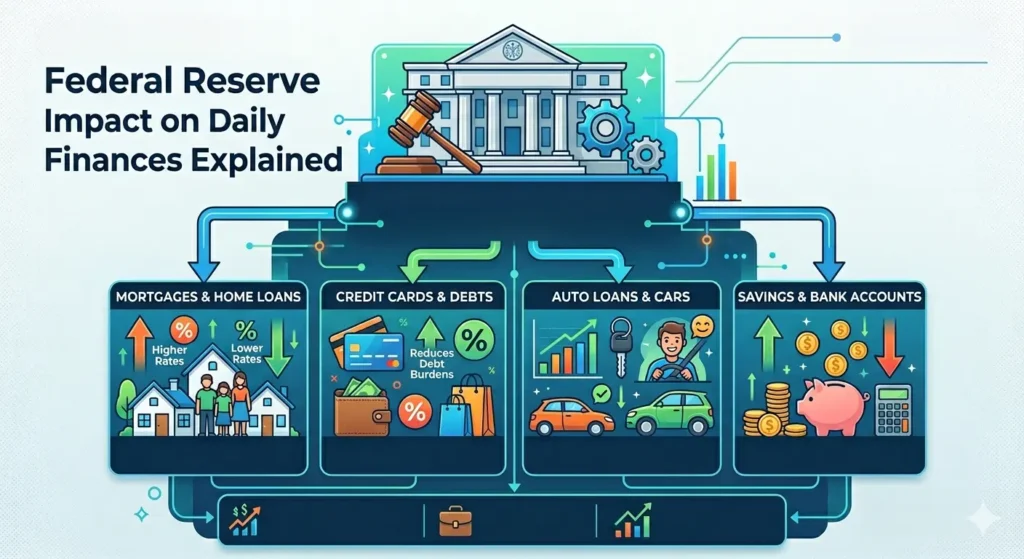

A small rate increase from the Fed can influence how much you pay for a home loan, how expensive car financing becomes, and even how much interest you earn on savings.

For buyers watching the housing market closely, understanding the Fed matters more than ever. Markets respond quickly when borrowing costs change. Buyer confidence shifts. Developers rethink pricing. Banks become stricter or more flexible with lending.

The Federal Reserve may not directly sell mortgages or build homes. However, its decisions shape the financial environment around them.

What Is the Federal Reserve?

The Federal Reserve, often called the Fed, is the central banking system of the United States. Its role is to support a stable economy.

It mainly focuses on three things:

- Controlling inflation

- Supporting employment

- Maintaining financial stability

One of its strongest tools is interest rates.

When inflation rises too quickly, the Fed usually raises interest rates to slow spending and borrowing. When the economy weakens, it may lower rates to encourage people and businesses to spend more.

Think about what happened during periods of economic slowdown. Borrowing became cheaper. Mortgage activity increased. More people entered the housing market because financing felt manageable.

That is how deeply the Fed can influence everyday life.

Why Interest Rates Affect Almost Everything

Interest rates shape the cost of borrowing money. This includes:

- Home loans

- Credit cards

- Auto financing

- Personal loans

- Business funding

When the Fed raises rates, banks usually raise borrowing costs too.

Imagine a family planning to buy a home in Texas. A mortgage that once felt affordable suddenly comes with a much higher monthly payment. That may force buyers to delay their purchase or look for smaller homes.

At the same time, businesses may slow hiring or expansion plans because financing becomes expensive.

However, there is another side to this.

Higher rates can benefit savers. Banks often increase returns on savings accounts and fixed deposits during these periods.

So while borrowers may feel pressure, savers sometimes gain an advantage.

The Connection Between the Fed and Mortgage Rates

Mortgage rates do not move exactly with Federal Reserve decisions. However, the Fed strongly influences the overall lending environment.

When investors expect higher inflation or tighter financial conditions, mortgage rates often rise as well.

Even a small increase can create a noticeable impact.

For example, consider a buyer taking a thirty year mortgage. A one percent increase in rates could add hundreds of dollars to monthly payments. Over time, that becomes a major financial difference.

Would that change the kind of property someone buys? In many cases, yes.

This is why real estate markets closely track every Federal Reserve meeting.

How Housing Markets React

Housing markets usually respond quickly when borrowing becomes expensive.

When financing costs rise:

- Buyer demand may slow

- Sellers may reduce prices

- Developers may delay projects

- Inventory may increase

Yet strong markets often continue attracting buyers despite higher rates.

Take cities like Austin, Miami, or Nashville as examples. These markets have continued attracting buyers because of job growth, infrastructure development, and strong housing demand.

Even during periods of higher interest rates, many buyers still see long-term value in these locations.

Credit Cards and Household Spending

Federal Reserve decisions also affect everyday spending habits.

Many credit cards have variable interest rates. So when the Fed raises rates, credit card interest usually rises too.

This can quietly increase financial pressure.

A person carrying a balance may suddenly notice larger monthly payments even if spending habits stay the same.

Have you noticed groceries, dining, and travel becoming more expensive while debt payments also rise? That combination often forces households to rethink budgets.

During higher rate periods, many families focus more on:

- Paying down debt

- Building emergency savings

- Avoiding unnecessary borrowing

- Choosing fixed rate loans when possible

These financial habits become especially important during uncertain economic conditions.

Also Check: Smart Money Habits That Prevent Costly Mistakes

Savings and Investments Also Change

Not every effect of higher rates is negative.

People with savings accounts often benefit because banks increase interest payouts. Retirees and conservative investors may also see better returns from safer financial products.

At the same time, stock markets can become more unpredictable. Businesses face higher borrowing costs and consumers often spend less.

Real estate investors also adjust strategies.

Some continue buying properties because rental demand remains strong. Others prefer waiting until financing conditions improve.

Every market cycle creates both risks and opportunities.

Why Inflation Matters So Much

Inflation affects nearly every household expense.

When prices rise too quickly, people pay more for groceries, fuel, healthcare, construction materials, and rent.

The Federal Reserve tries to slow inflation by reducing excess spending across the economy.

Higher interest rates are designed to cool demand gradually.

However, balancing inflation without hurting economic growth is challenging. Raise rates too aggressively and economic activity may slow sharply. Move too slowly and inflation may remain high for longer.

This is why investors, businesses, and homebuyers closely watch inflation reports and Fed announcements.

Also Check: How Inflation Impacts Everyday Household Budgets

What Homebuyers Should Pay Attention To

If you are planning to buy a home, following Federal Reserve trends can help you make better financial decisions.

Some important things to watch include:

- Inflation levels

- Mortgage rate trends

- Housing inventory

- Employment conditions

- Consumer confidence

At the same time, trying to perfectly predict the market rarely works.

A more practical approach is to focus on affordability and long term financial comfort.

Ask yourself simple questions:

- Can I comfortably manage the monthly payment?

- Does this purchase fit my future plans?

- Am I financially prepared for unexpected expenses?

These questions matter more than short-term market noise.

Also Read: First-Time Homebuyer Programs You Should Know

The Bigger Financial Picture

The Federal Reserve does not directly control your wallet. Yet its decisions shape the financial system surrounding your daily life.

From mortgage approvals and home affordability to savings returns and credit card costs, its influence appears almost everywhere.

Understanding how the Fed works can help consumers feel more confident during uncertain economic periods. It can also help homebuyers make smarter decisions instead of reacting emotionally to headlines.

And as global real estate markets become more connected, staying informed is no longer just useful. It is necessary.